In the wake of social unrest and a global pandemic, investors are taking a closer look at how asset managers are evaluating “social” risk and opportunity. While the current environment has raised the profile of many social factors, workforce diversity, equity and inclusion (DEI), in particular, is finally getting the attention it deserves. How companies manage DEI may have a material impact on their ability to attract and retain employees, and clients which may ultimately affect their financial performance. Asset managers need a structured way to evaluate their investments on this dimension, but that isn’t enough. Managers also need to turn the mirror on themselves and examine their own practices and align the two.

Accelerating initiatives on DEI is an imperative. Ultimately organizations should be doing this because it is the right thing to do. But, there are numerous studies that support the correlation with the financial benefits. The strategy for building DEI requires the attention of executives and directors to ensure the recruiting pipeline is focused on diverse talent early in the process — and early in an individual’s career — complete with a process that encourages the promotion, equitable pay, and engagement of diverse talent throughout the organization. The payoff is more than worth the effort: Workforce diversity – especially among leadership – correlates with increased financial performance. This finding is evidenced by recent analyses by both BCG and McKinsey, that suggest asset managers, and the companies in which they invest, stand to benefit from diverse leadership.

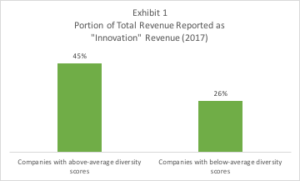

Diversity supports innovation and can position those companies for growth. The BCG study found companies with above average diversity scores generate on average 45% of their revenue from “innovation” sources (products and services launched within the preceding three years) vs 26% from those with below average scores (Exhibit 1).

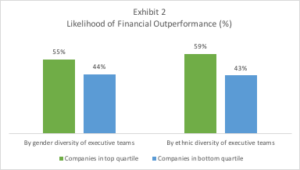

This can translate into financial outperformance according to the McKinsey report (Exhibit 2), with organizations having more gender and ethnic diversity at the executive level more likely to outperform less diverse organizations by more than ten percentage points.

Pressure to enhance workforce diversity is building among investors, as well as legislative bodies. In July 2020, the New York City Comptroller requested that 67 S&P 100 companies which had issued statements in support of racial equality disclose employment data or face shareholder proposals in 2021. Workforce diversity was a key engagement topic for investors in 2020, as observed by the EY Center for Board Matters.

In addition, legislation has been introduced mandating diverse board representation, starting with Norway in 2003. In September 2020, California passed a law mandating that publicly traded companies within the state have at least one racially, ethnically, or otherwise diverse member on the board of directors by 2021– following up on a 2018 law mandating female directors on boards. New Jersey and Michigan have formulated bills mandating female representation on boards, while Illinois, Maryland, and New York are seeking disclosure on board gender diversity.

Asset managers should incorporate a formal assessment in their research process to determine how an investment is managing DEI, and whether their actions may present a risk or advantage. Some topics to evaluate include:

- How does the organization approach DEI? Does it disclose its approach and does it have goals?

- Does the board have formal oversight of DEI and what information do they review?

- Are they disclosing workforce information, including data for all levels of staff, and not just executives?

- What action is the organization taking to build a more diverse workforce, and importantly, what action is it taking to ensure it engages its diverse employees and gives them opportunities to advance?

- What is the organization’s turnover and is it higher or lower than the industry, and may that be an indication of how they are managing their diversity efforts?

Similarly, asset owners can evaluate their asset managers on the same issues noted above, and also determine if the manager’s approach to DEI in their investments is aligned with their own corporate practices, policies and disclosures, by asking:

- How does the manager approach DEI for their organization and is it aligned with their investment approach?

- Does it have a formal process to evaluate the DEI efforts of its investments?

- How is DEI incorporated into its proxy voting policy, and importantly, into its proxy voting decisions. Has it set specific targets to drive change and does its voting record hold companies accountable?

- What is its approach to engagement to influence organizations to address this issue?

DEI is ever more important for asset managers and asset owners to systematically address –to satisfy the demands of all their stakeholders, to attract and retain talent, and ultimately contribute to the firm’s success. It will become evident which asset managers are committed to DEI, or not, through their actions. Those who are simply greenwashing will stand out and be called out.